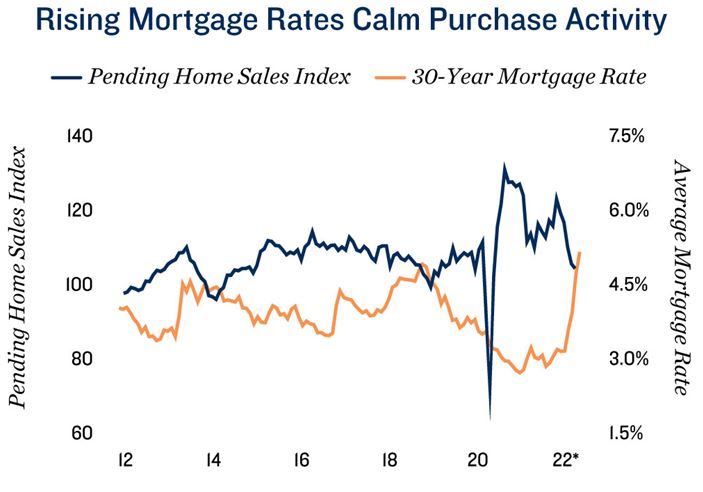

Pending home sales reveal impact of mortgage rate surge. Upward pressure on mortgage rates from lofty inflation and the Fed’s plan to hike interest rates multiple times this year are influencing home buying. In late April, the average rate for a 30-year mortgage climbed for the seventh consecutive week to 5.1 percent, up 200 basis points from the beginning of this year and almost twice as high as the 2020 trough. While demand for homes remains sturdy, the higher cost of borrowing is condensing buying activity. The pending home sales index illustrates this trend, with the March measure the lowest since early 2020 and 8 percent beneath the recording one year prior. A slowdown in purchases, however, has not yet weighed on price growth. The median sale price of an existing home rose 1.3 percent month-over-month in March.

Pending home sales reveal impact of mortgage rate surge. Upward pressure on mortgage rates from lofty inflation and the Fed’s plan to hike interest rates multiple times this year are influencing home buying. In late April, the average rate for a 30-year mortgage climbed for the seventh consecutive week to 5.1 percent, up 200 basis points from the beginning of this year and almost twice as high as the 2020 trough. While demand for homes remains sturdy, the higher cost of borrowing is condensing buying activity. The pending home sales index illustrates this trend, with the March measure the lowest since early 2020 and 8 percent beneath the recording one year prior. A slowdown in purchases, however, has not yet weighed on price growth. The median sale price of an existing home rose 1.3 percent month-over-month in March.

Multifamily still in a strong position if housing market cools. The recent mortgage rate swell and coinciding moderation of home purchases has the potential to temper price growth, but the affordability gap relative to apartments remains substantial. The difference between an average monthly mortgage payment and a rent obligation stood at $638 in the first quarter of 2022. By comparison, that margin was $440 during the same period in 2021. Not only do apartments appeal as a significantly more affordable living option, they also offer greater flexibility via short-term leases, require little maintenance by tenants and sometimes provide attractive amenities, such as workout facilities and pools. These factors will sustain multifamily momentum, keeping the national vacancy rate extremely tight in the mid-2 percent range in 2022.

Mortgage rate climb pushes demand toward luxury rentals. Higher-end apartments are poised to benefit in the new mortgage rate climate. Growth in the professional and business services and financial activities segments, which typically offer above-average wages, is enlarging the prospective renter pool. In prior years, this grouping may have been inclined to purchase a home, but elevated borrowing costs, paired with high prices, are making this difficult. Low Class A vacancy amid demand tailwinds should forge the conditions for the record supply wave to be well received this year.

Number of homes for sale ticks up. In March, existing home listings rose month-over-month, which had not happened since July of last year. This may indicate that some owners waiting to list amid fast appreciation were coaxed into selling as mortgage rates started to rise. The opportunity to lock in favorable financing on a home they plan on moving to before rates increased further was a motivating factor, while expectations for additional appreciation may be subsiding as purchase activity tapers. This is a step toward cooling the supply-demand imbalance, but the for-sale count is still minute historically. The 890,000 existing homes listed in March is below every month between 1982 and 2021.

Costs of new homes skyrocket, despite fewer purchases. The median price of a newly built single-family house reached $443,000 in March, escalating by more than 4 percent from February. During the same month, the number of new homes for sale notched a 13-year high, while the amount of these dwellings sold dropped to a four-month low. If these trends persist, upward pressure on newly built home prices could wane.