Leasing volumes robust. After encountering a disproportionate number of hurdles in 2020 and early 2021, apartment demand has soared in the nation’s gateway metros. During recent months, New York, Los Angeles and Chicago challenged Sun Belt and Mountain/Desert hot spot metros like Dallas-Fort Worth, Houston and Phoenix for the country’s largest increases in occupied units.

Leasing volumes robust. After encountering a disproportionate number of hurdles in 2020 and early 2021, apartment demand has soared in the nation’s gateway metros. During recent months, New York, Los Angeles and Chicago challenged Sun Belt and Mountain/Desert hot spot metros like Dallas-Fort Worth, Houston and Phoenix for the country’s largest increases in occupied units.

Sizable job creation fuels renter demand. Most gateway markets are now registering notable employment growth. Across the six major gateway metros, headcounts expanded by an average of 6.2 percent year-over-year in March, compared to 4.5 percent for the U.S. overall. Additions include a range of trades and service roles, as well as a mix of office-based jobs, work-from-home positions and hybrid employment situations. In turn, there is solid new household formation, particularly among young adults who have traditionally been attracted to gateway markets for their amenities and lifestyle characteristics. While some people who left these areas a year or two ago are returning, that is not the primary source of current apartment demand here.

The locations that gained households moving from gateway metros in 2020 are not suffering resident loss, on net, at this point.

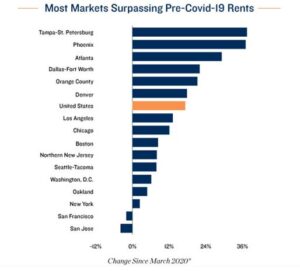

Rents rise above pre-pandemic levels. The annual growth pace for effective rents surged to 17.6 percent in Chicago during early 2022, moving past the hefty U.S. norm of 16.8 percent. Boston, Washington, D.C., Los Angeles and parts of the Bay Area posted year-over-year pricing increases in the 10 percent to 18 percent range, similar to the national average. Rent growth over the past year more than countered earlier cuts and pushed pricing to new highs in most gateway market locations. Rents as of the first quarter are 12 percent to 13 percent above early 2020 pre-pandemic prices in Los Angeles and Chicago. Overall increases in the range of roughly 5 percent to 8 percent registered in

Boston and Washington, D.C., as well as in the gateway adjacent metros of Northern New Jersey and Oakland. A bump of just over 2 percent was seen in New York. In contrast, rents were still 2 percent under early 2020 prices in San Francisco, while San Jose’s average monthly rates trailed the past high by 3.9 percent.

Room left for further substantial upward rent movement. While improving rents in gateway metros is encouraging, these markets still lag most of the country in performance over the past two years. All six of the major metros in this category posted two-year rent increases below the 17.3 percent U.S. average, and fell well short of the pricing jumps of more than 30 percent recorded in several key Florida markets, as well as Phoenix, Las Vegas and Riverside-San Bernardino.

Momentum set to shift to gateway markets. Looking ahead, gateway metros should maintain higher rent growth momentum relative to the country as a whole or today’s best performing metros. Monthly rates have yet to jump significantly in most gateway markets relative to what is occurring in some other locations where new residents are filing in more rapidly. Furthermore, none of the gateway metros have vacancy issues or outsized construction activity that could derail returning momentum for rent growth results.